Your 7 Most Common Centrelink Questions at Retirement

By Max Grant.

Let’s face it, Centrelink can be a nightmare to deal with. If waiting on hold for up to an hour or going to your local branch wasn’t hard enough, try navigating some of the complex definitions and thresholds that change on a regular basis.

Yes, it’s fair to say Centrelink has more rule changes than the AFL. We get a constant stream of questions regarding Australia’s favourite institution and what you might be eligible for as you close in on retirement.

In response, we decided to put together a list of our top seven Centrelink FAQs to help build your knowledge and know your rights when it comes to the subject of retirement and Centrelink.

Here they are from one to seven:

1. Am I eligible for an Age Pension from Centrelink?

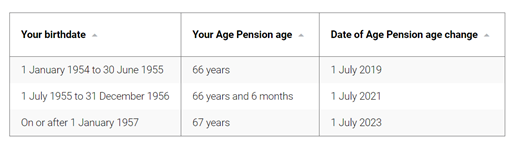

To be eligible you must be a certain age* and depending on your circumstances be under or within certain Asset and Income testing thresholds. At the very least, to be eligible for Age Pension you must be 66 or older.

Here is a table demonstrating how Age Pension age is currently increasing according to when you were born:

* Despite what you might hear or read, there’s no such thing as a ‘retirement age’ in Australia, nor any laws that dictate when someone can retire. In theory, you can choose to retire whenever you want if you have the financial resources to afford it.

In practice, there are two age rules that impact when most Australians can retire because they allow you to access funds to support your retirement. These are:

Preservation age: This is the age when you can access your super provided you have also met a condition of release (such as retiring or turning 65).

Age Pension age: This is the age when you can access Australia’s Age Pension, provided you’re an Australian resident and you qualify under the income test and the assets test.

2. How much can I gift before my payment is affected?

You can gift $30,000 over any 5-year rolling financial year period, with a maximum of $10k per financial year without your Centrelink payment/entitlement being affected.

If you or your partner gift money, income, or assets, over this amount Centrelink may assess it as an asset for a period of 5 years.

Before you or your partner make a gift, it could be wise to contact Centrelink, or your financial adviser, to check how it will affect your payment.

3. As a self-funded retiree, is there anything other than the Age Pension I could be eligible for?

For those that are Age Pension age and do not qualify for a pension, you could be eligible for a Low-Income Health Care Card or Commonwealth Seniors Health Card (or both).

Check the current income test on the Services Australia website for more about the income test for a Low-Income Healthcare Card and whether you qualify. It is important to note that you can be any age and be eligible for a Low-Income Health Care Card

You must be Age Pension age to receive a Commonwealth Seniors Health Care Card in addition to meeting a few other criteria.

4. What benefits do I get from the Low-Income Health Care Card?

Most of the benefits are the same as the Pensioner Concession Card, though as holder of the Pensioner Concession Card you get a discount on your rates notice and an additional discount on the cost of your motor vehicle registration.

The benefits you will receive as a holder of the Low-Income Health Care Card include:

- Cheaper medicine under the Pharmaceutical Benefits Scheme

- Bulk billed doctor visits (this is up to your doctor)

- A bigger refund for medical costs when you reach the Medicare Safety Net.

Your state or territory government and local council may offer you more. They may lower your:

- electricity and gas bills

- property and water rates

- public transport fare

- motor vehicle registration.

Whilst it does not sound extravagant, we find our self-funded retirees to be grateful for the discounts the card provides.

5. How does my partner’s assets and income affect my Age Pension payment?

For Age Pension purposes your partners assets and income will be used to determine your entitlement. Generally, all assets are assessable but there are some exemptions. For example, a common (mostly unknown) exemption is that superannuation held in accumulation phase whilst you are under Age Pension age is not assessable for Centrelink testing purposes.

6. Do Centrelink know all my information and how often do I need to update Centrelink?

Centrelink will ask a lot of personal questions, but they do not know what is happening with your finances on a day-to-day basis. It is your job to notify Centrelink within 14 days of any significant changes in your personal financial circumstances.

When you undertake an application, Centrelink will ask you for some documents to support your claim for a payment or concession card. It does not have the power to spot check your bank accounts as some people claim.

7. Can somebody do all this Centrelink stuff for me?

Yes, you have the option of implementing a nominee arrangement. Muirfield finds that our clients appreciate the option of nominating us as a correspondence nominee to assist with the management of their Centrelink payments and concessions.

This ensures that any applications, updates, or problems are handled in the most efficient and effective way possible.

Contact us if you would like to discuss how we can help with Centrelink and your retirement.

There are lots of nuts and bolts when it comes to Centrelink and knowing what you’re eligible for, but the process for claiming payments and concessions can be straightforward once you’re all set up.

My wife and I are considering making an appointment for some advise from Muirfield, we’ve had some positive comments about your firm from a number of friends. We will contact you once the current lockdown is over and we’ve finalised our 2020/21 tax returns.

Your information pages have been very informative and we look forward to making an appointment in the very near future.

Thanks for reaching out Tony and Jenni, it’s always nice to hear some positive feedback. Let’s hope the lockdown lifts and we can have you in for a face-to-face meeting soon.

In the meantime I’d be more than happy to answer your immediate questions over the phone. You can call our office on 03 5224 2700.

All the best

Courtney Robinson.

Hi, I’m an aussie citerzen, living in the UK. But I want to return to Australia PERMENTLY. Would I be able to get age pension immediately? Hope you can help, I’ve tried everywhere, but can’t find the answer online. Kind regards Julie

Hi Julie,

By the sounds of it you meet the residency requirements to be eligible for the Age Pension. There are many other rules to consider when determining your eligibility. You can find more information here https://www.servicesaustralia.gov.au/individuals/services/centrelink/age-pension/who-can-get-it/residence-rules.

All the best

Courtney

Hi

Have read that payments from a close relative are not assessable as income under pension rules

Please advise how this works?

Hi Gary,

This is very much a grey area, it depends what the payments constitute. We cannot provide you with a clearer answer without more information.

Thanks

The Muirfield Team

Hi and Thank You in Advance for your reply. I am 70 years of age, will be 71 later this year. I still worked up until 2/7/2021 and retired 4/10/2021 was paid weekly long service leave and annual leave during this period, NO lump sum payments. Easy job night shift. Age pension has been paid since 4/10/2021. I was injured in an accident (not at work) in June 2018, local hospital misdiagnosed a major issue and have admitted fault. Admitted liability and are making a settlement offer in June 2022 sum after expenses expected to be $300000. My first payment from Centrelink was 4/10/2021 nothing before that date, ever. I understand Centrelink will require that money paid back, thats OK, plus I know there will be an exclusion period from settlement date. Have my own home owe approx $150000, market value $350000, no super money it was used to settle bills, small amount in bank, owe two older cars $10000 total value of both. Are you able to advise how Centrelink work out their numbers on these figures, and should I pay off the mortgage balance. Regards

Hi Richard,

Thanks for your questions. Given your questions are quite specific they are beyond the scope of this forum.

If you would like to chat to one of our advisers, please call our office on 03 5224 2700.

All the best

Hi I have a general question about testamery trusts and centrelink assessment of distributions.

I have some shares from my parents estate held in a testamery trust. Centrelink has assessed me as 100% attributable stakeholder and treats the shares as mine.

When selling the shares a considerable capital gains tax will be paid and the liability for the tax will be distributed to me. The proceeds of the sale will be added to my assets. Will Centrelink count the capital gain as income?

Hi Anne,

The capital gain will not be considered income from Centrelink’s perspective.

Shares are considered a financial asset, therefore, Centrelink calculate income via the “deeming” rules.

Please refer to our earlier articles about deeming for more information.

Take care

Courtney Robinson

Hi, I am retiring at the end of this year. I will receive about 14 weeks LSL pay in my final termination lump sum payment. The question is, my wife is already pension age and can receive the pension as soon as I retire. Will her payment be held up until the end of the 14 weeks of LSL pay that I receive as a lump sum, or will she start getting the pension straight away after my final day.

Hi Joe,

If you are referring to the Age Pension, then no, waiting periods do not apply to this payment.

Assuming your leave payout is left in the bank, it will count towards the asset test and be deemed to earn income under the income test.

I trust this answers your question.

Take care.

Courtney Robinson

How much mo ey can I have in the Bank and not effect my pension if I do not own a home

Hi Sue,

The answer depends on your circumstances. We will soon publish an article which covers this topic.

Keep an eye out.

All the best

Muirfield

Hi David here

I have recently sold my business and i havnt got a house.

My wife is 42 and i am 69.

We intend to move to a regional area as housing is cheaper.

I intend to go on the aged pension,is my wife elegible for any benefit until she finds a job.

Hi David,

Without knowing your full financial and personal circumstances, we cannot make an assessment of you or your wife’s eligibility for a benefit.

Generally speaking, Jobseeker Allowance is commonly used for people who are unable to work prior to reaching Age Pension age.

I hope that points you in the right direction.

Take care.

Muirfield

My wife and I are on a full aged pension but we would like to work, Can you tell me how much each year we can each earn before our age pension is affected

Hi Brian,

Great question. Centrelink have what’s called a work bonus which means the first $300pf you earn from employment is not counted towards your income assessment.

I hope that helps.

All the best

Muirfield

Hi, my partner and I are on the aged pension.

we recently have contracted to sell our shack.

we sold it for 300,000.

About 15,000 will go in real estate marketing and legal fees.

Of the remainder we will pay remaining mortgage on shack and home.

we estimate about 80,000 remaining.

We understand we can have that in the bank for up to two years to downsize or do renovations but also that it is classed as income. will it affect our fortnightly payment?

Hi Elizabeth, thanks for the question.

By the sounds of it your “shack” was a holiday home of sorts and you have another home as your principal residence.

If this is the case, the two year asset test exemption does not apply to the proceeds from your shack.

I hope this helps.

The Muirfield Team

we are applying for the aged pension our property area is 2.19 hectares that is 0.19 larger than allowed we live in a rural living area and our local council does not allow subdivision without state government changes We cannot sell that 0.19 hectares or a larger portion of our property . Centerlink wants to know what value it has . As far as we cans it has no value as we cannot sell it . Any ideas