The myth about super fees

In April of this year Super Ratings released a research article stating that lower fees had little correlation with fund performance and overall retirement outcomes. The article went on to explain that although fees do impact the bottom line, the overall value delivered by a super fund cannot be determined without also considering investment performance, insurance offerings, administrative capabilities and member services.

It makes sense, lower fees do not necessarily mean good returns and great service. To an extent it plays to the age old adage, you get what you pay for.

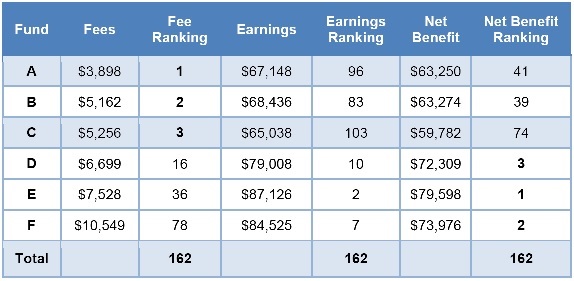

To explain it more clearly Super Ratings provided a table of fees versus net benefit.

(Fees and Earnings are the aggregate amounts over the 10 year period)

It is clear to see that the funds which ranked highest for low fees tended to underperform when it came to investment earnings. Conversely the funds that charged more delivered better investment returns and gave a better net result to clients even after taking into account fees.

Quality advice from a financial adviser also ties into this argument given it can help improve the benefit experienced by a client. Although costs once again come into question, appropriately tailored financial advice can help both reduce tax, increase wealth and deliver peace of mind, something than cannot be understated. These benefits more often than not far exceed the cost of advice.

This is not to say price shouldn’t enter the argument when choosing a super fund and financial advice, rather price should only form part of your decision and not in isolation of the other benefits provided.

The research findings in this article were conducted by Super Ratings, an impartial superannuation ratings house. To read the full article please follow this link.